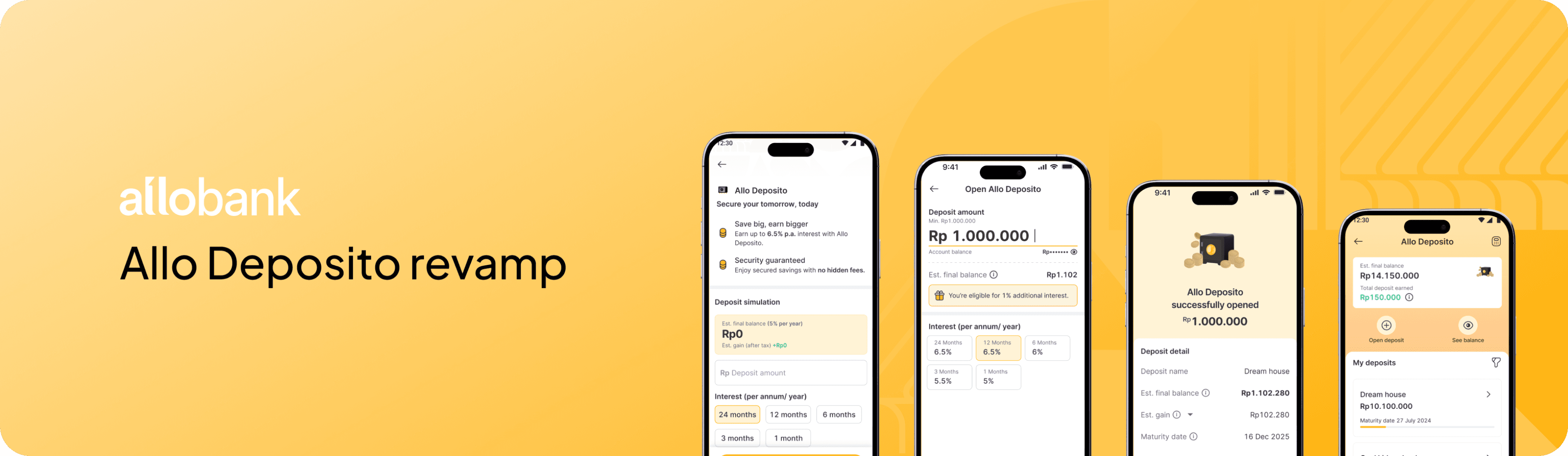

Allo Deposito revamp

Allo Deposito revamp

Background

Background

Background

Allo Deposito, a key feature in Allo Bank's marketing campaigns, has struggled with low account adoption rates despite its importance. To address this, I proposed a revamp to enhance usability, improve the user experience, and implement a fresh UI using our new design system, making the feature more engaging and user-friendly.

Allo Deposito, a key feature in Allo Bank's marketing campaigns, has struggled with low account adoption rates despite its importance. To address this, I proposed a revamp to enhance usability, improve the user experience, and implement a fresh UI using our new design system, making the feature more engaging and user-friendly.

Allo Deposito, a key feature in Allo Bank's marketing campaigns, has struggled with low account adoption rates despite its importance. To address this, I proposed a revamp to enhance usability, improve the user experience, and implement a fresh UI using our new design system, making the feature more engaging and user-friendly.

Data findings

Data findings

Data findings

Currently, Allo Deposito has only 10,000 active deposit accounts, representing just 1% of our 1 million active users. This highlights a significant gap in user engagement with the feature. To address this, we aim to increase the number of active deposit users by 20-30% in 2025.

Currently, Allo Deposito has only 10,000 active deposit accounts, representing just 1% of our 1 million active users. This highlights a significant gap in user engagement with the feature. To address this, we aim to increase the number of active deposit users by 20-30% in 2025.

Currently, Allo Deposito has only 10,000 active deposit accounts, representing just 1% of our 1 million active users. This highlights a significant gap in user engagement with the feature. To address this, we aim to increase the number of active deposit users by 20-30% in 2025.

Design process

Design process

Design process

We follow proper design process to give the best design solution.

We follow proper design process to give the best design solution.

We follow proper design process to give the best design solution.

Establish requirement

Establish requirement

Establish requirement

Build prototype

Build prototype

Design alternatives

Design alternatives

Design alternatives

Evaluate design

Evaluate design

Evaluate design

Build prototype

Surveys and quantitative research

Surveys and quantitative research

Surveys and quantitative research

With support from the research team, we conducted a quantitative study involving 166 users who either use Allo Deposito or deposit with other banks. Here are the key insights we gathered:

With support from the research team, we conducted a quantitative study involving 166 users who either use Allo Deposito or deposit with other banks. Here are the key insights we gathered:

With support from the research team, we conducted a quantitative study involving 166 users who either use Allo Deposito or deposit with other banks. Here are the key insights we gathered:

Where they put their money?

Where they put their money?

Where they put their money?

Other than Allo Bank

Other than Allo Bank

Other than Allo Bank

Seabank

Seabank

Seabank

34%

34%

34%

BNC

BNC

BNC

27%

27%

27%

BCA

BCA

BCA

25%

25%

25%

Mandiri

Mandiri

Mandiri

34%

34%

34%

Easiest product to understand

Easiest product to understand

Easiest product to understand

Other than Allo Bank

Other than Allo Bank

Other than Allo Bank

BNC

BNC

BNC

1st

1st

1st

Seabank

Seabank

Seabank

2nd

2nd

2nd

BCA

BCA

BCA

3rd

3rd

3rd

BRI

BRI

BRI

4th

4th

4th

Most profitable deposit

Most profitable deposit

Most profitable deposit

Other than Allo Bank

Other than Allo Bank

Other than Allo Bank

Seabank

Seabank

Seabank

34%

34%

34%

BNC

BNC

BNC

27%

27%

27%

Superbank

Superbank

Superbank

25%

25%

25%

Jago

Jago

Jago

34%

34%

34%

Barriers when planning to invest

Barriers when planning to invest

Barriers when planning to invest

Incomplete & unclear product info

Incomplete & unclear product info

Incomplete & unclear product info

(28%)

(28%)

(28%)

Difficult interest calculation simulation

Difficult interest calculation simulation

Difficult interest calculation simulation

(24%)

(24%)

(24%)

High break deposit fees

High break deposit fees

High break deposit fees

(22%)

(22%)

(22%)

Terms and abbreviations issue

Terms and abbreviations issue

Terms and abbreviations issue

Most of banking term are not instantly understandable to our users.

Most of banking term are not instantly understandable to our users.

Most of banking term are not instantly understandable to our users.

Maturity notification

Maturity notification

Maturity notification

Whenever a deposit almost/already reach its maturity date, our user never receive any notification.

Whenever a deposit almost/already reach its maturity date, our user never receive any notification.

Whenever a deposit almost/already reach its maturity date, our user never receive any notification.

Early break consequences

Early break consequences

Early break consequences

Information regarding early break aren’t shown/given in clear.

Information regarding early break aren’t shown/given in clear.

Information regarding early break aren’t shown/given in clear.

Readability and hierarchy issue

Readability and hierarchy issue

Readability and hierarchy issue

Information hierarchy and placement are not in desired way. Font size also inconvenient to read.

Information hierarchy and placement are not in desired way. Font size also inconvenient to read.

Information hierarchy and placement are not in desired way. Font size also inconvenient to read.

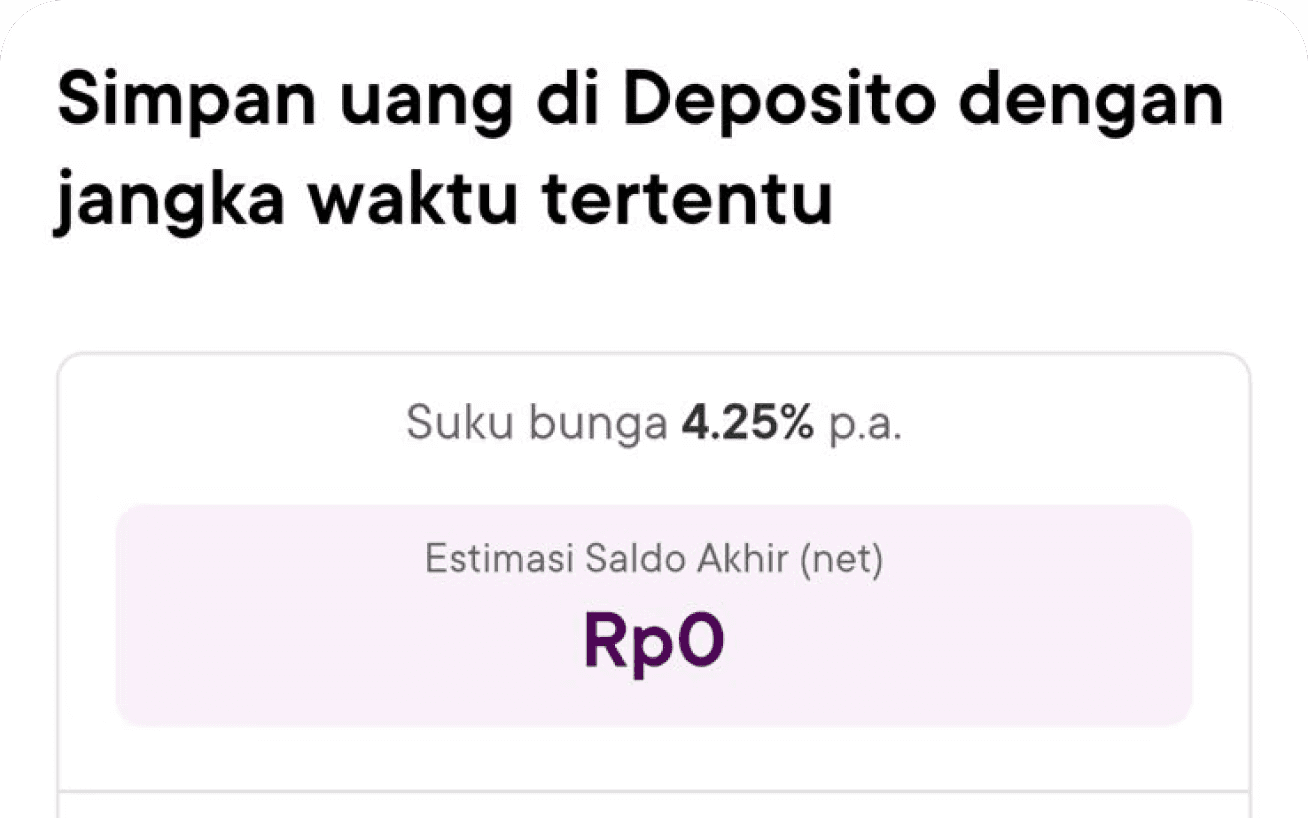

Competitor reference

Competitor reference

Competitor reference

I conducted a competitor analysis focused on the processes for opening and early breaking deposits. The digital banks analyzed included Bank Jago, Krom Bank, Bank Saqu, and Superbank. Below is a summary of the pros and cons observed:

I conducted a competitor analysis focused on the processes for opening and early breaking deposits. The digital banks analyzed included Bank Jago, Krom Bank, Bank Saqu, and Superbank. Below is a summary of the pros and cons observed:

I conducted a competitor analysis focused on the processes for opening and early breaking deposits. The digital banks analyzed included Bank Jago, Krom Bank, Bank Saqu, and Superbank. Below is a summary of the pros and cons observed:

Delightful User Interface screens.

Deposit maturity countdown time.

Seamless opening flow.

Deposit rate for each maturity term doesn’t shown directly.

High minimum deposit amount (Rp1.000.000).

Quick simulation (use Rp10.000.00 deposit amount simulation).

Flexibility to select maturity date on any date.

Deposit maturity countdown time.

Deposit rate for each maturity term doesn't shown directly.

Somewhat not seamless opening flow.

They have a unique deposit product called Busposito

Interest not directly shown in opening page.

Regular deposit product seems less highlighted compared to Busposito.

Interest gained aren't shown directly when user input deposit amount.

Informative onboarding page. It shows short yet concise USPs.

Wide maturity date variation.

Basic FAQ section.

It only shows interest table, not interest simulation.

Delightful User Interface screens.

Deposit maturity countdown time.

Seamless opening flow.

Deposit rate for each maturity term doesn’t shown directly.

High minimum deposit amount (Rp1.000.000).

Quick simulation (use Rp10.000.00 deposit amount simulation).

Flexibility to select maturity date on any date.

Deposit maturity countdown time.

Deposit rate for each maturity term doesn't shown directly.

Somewhat not seamless opening flow.

They have a unique deposit product called Busposito

Interest not directly shown in opening page.

Regular deposit product seems less highlighted compared to Busposito.

Interest gained aren't shown directly when user input deposit amount.

Informative onboarding page. It shows short yet concise USPs.

Wide maturity date variation.

Basic FAQ section.

It only shows interest table, not interest simulation.

Opportunity Solution Tree

Opportunity Solution Tree

Opportunity Solution Tree

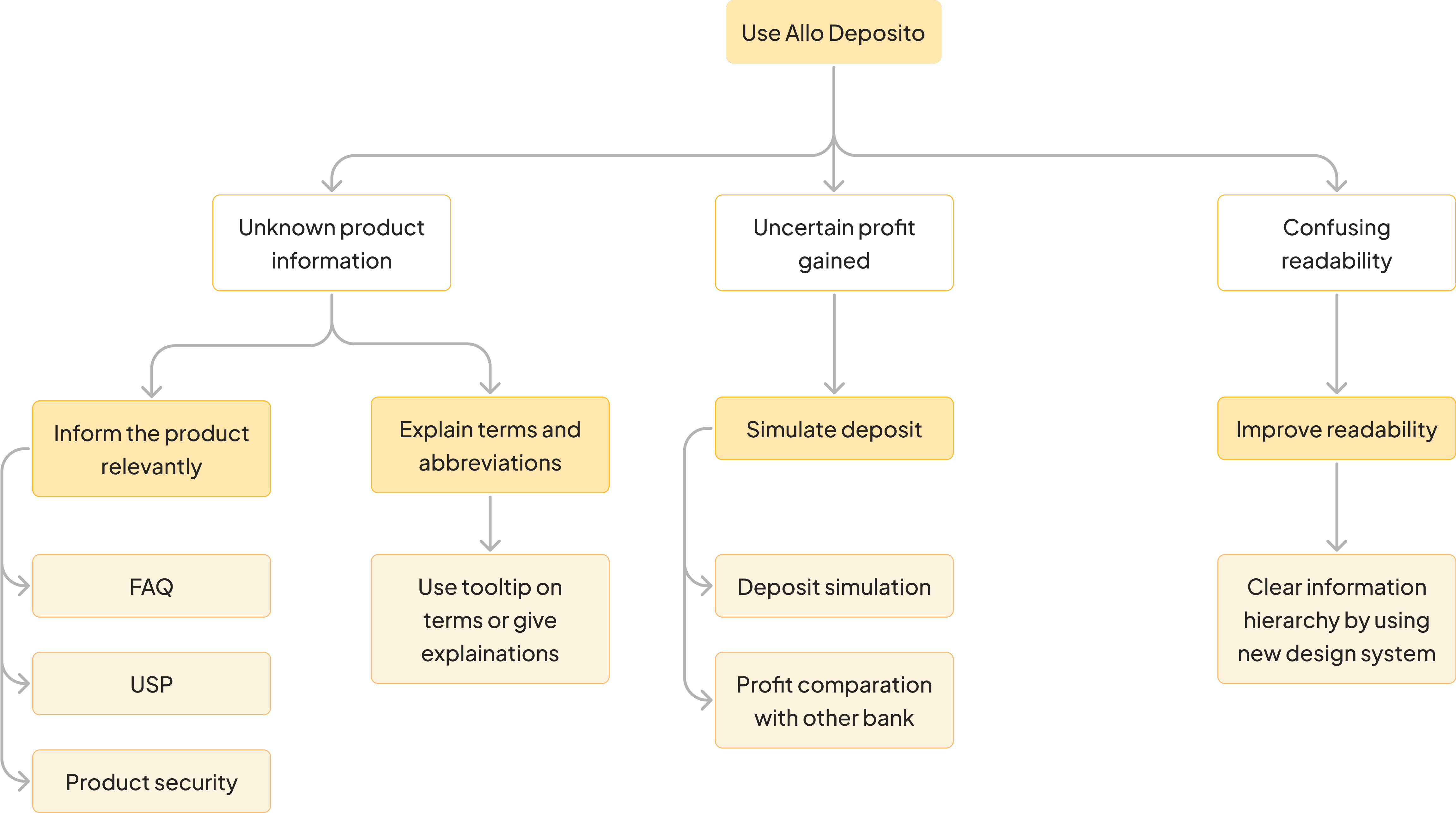

Based on synthesized insights from the research team and competitor analysis, I identified key opportunities to improve Allo Deposito and proposed several enhancements and experiments for the revamp. Below is the Opportunity Solution Tree outlining these proposals:

Based on synthesized insights from the research team and competitor analysis, I identified key opportunities to improve Allo Deposito and proposed several enhancements and experiments for the revamp. Below is the Opportunity Solution Tree outlining these proposals:

Based on synthesized insights from the research team and competitor analysis, I identified key opportunities to improve Allo Deposito and proposed several enhancements and experiments for the revamp. Below is the Opportunity Solution Tree outlining these proposals:

User flow

User flow

User flow

The revamped user flow focuses on two main use cases: deposit opening and early break flow. These flows have been optimized to enhance usability and address pain points identified during research. Below is the detailed flowchart for both use cases:

The revamped user flow focuses on two main use cases: deposit opening and early break flow. These flows have been optimized to enhance usability and address pain points identified during research. Below is the detailed flowchart for both use cases:

The revamped user flow focuses on two main use cases: deposit opening and early break flow. These flows have been optimized to enhance usability and address pain points identified during research. Below is the detailed flowchart for both use cases:

Allo Deposito opening

Allo Deposito opening

Allo Deposito opening

Early break

Early break

Early break

UI Screens

UI Screens

UI Screens

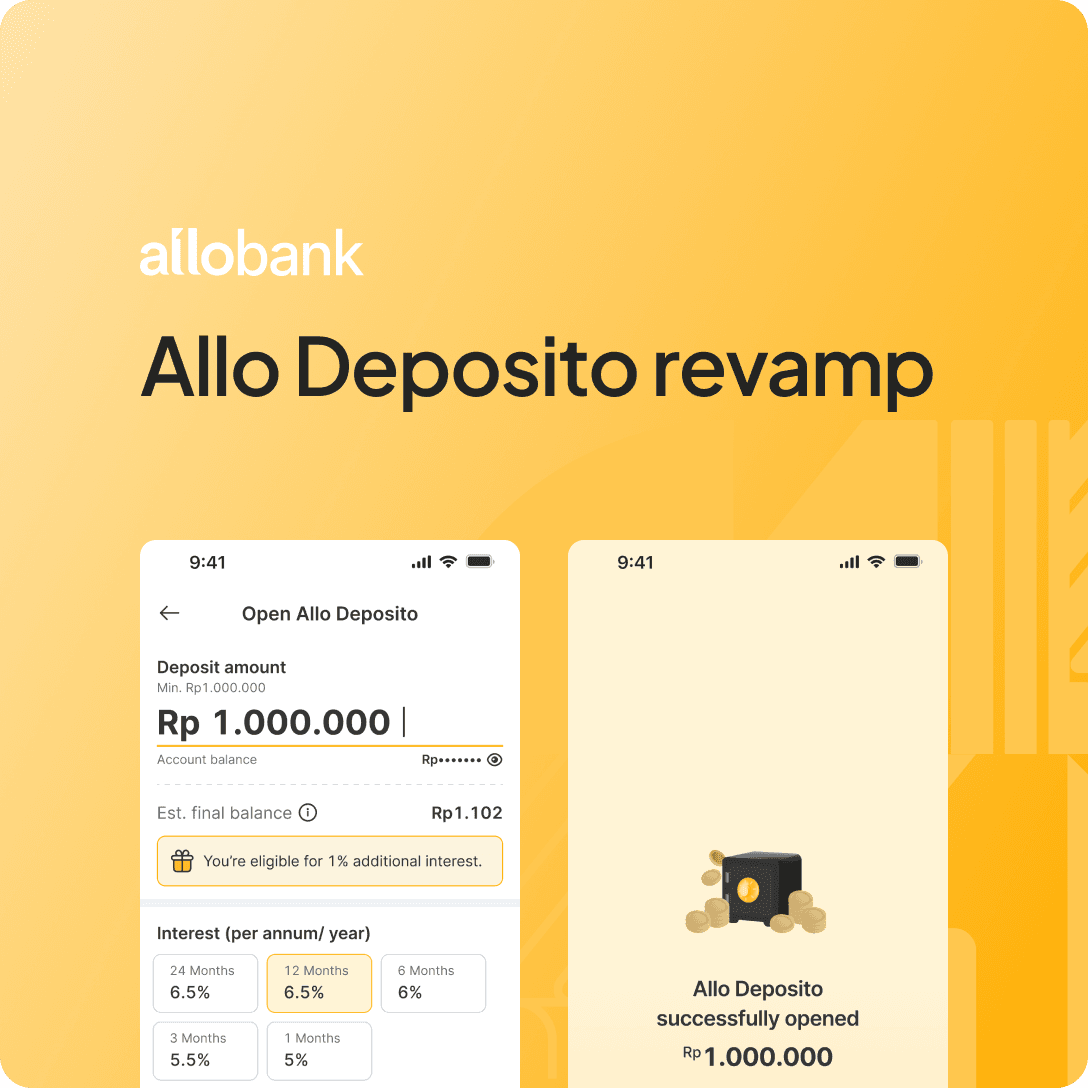

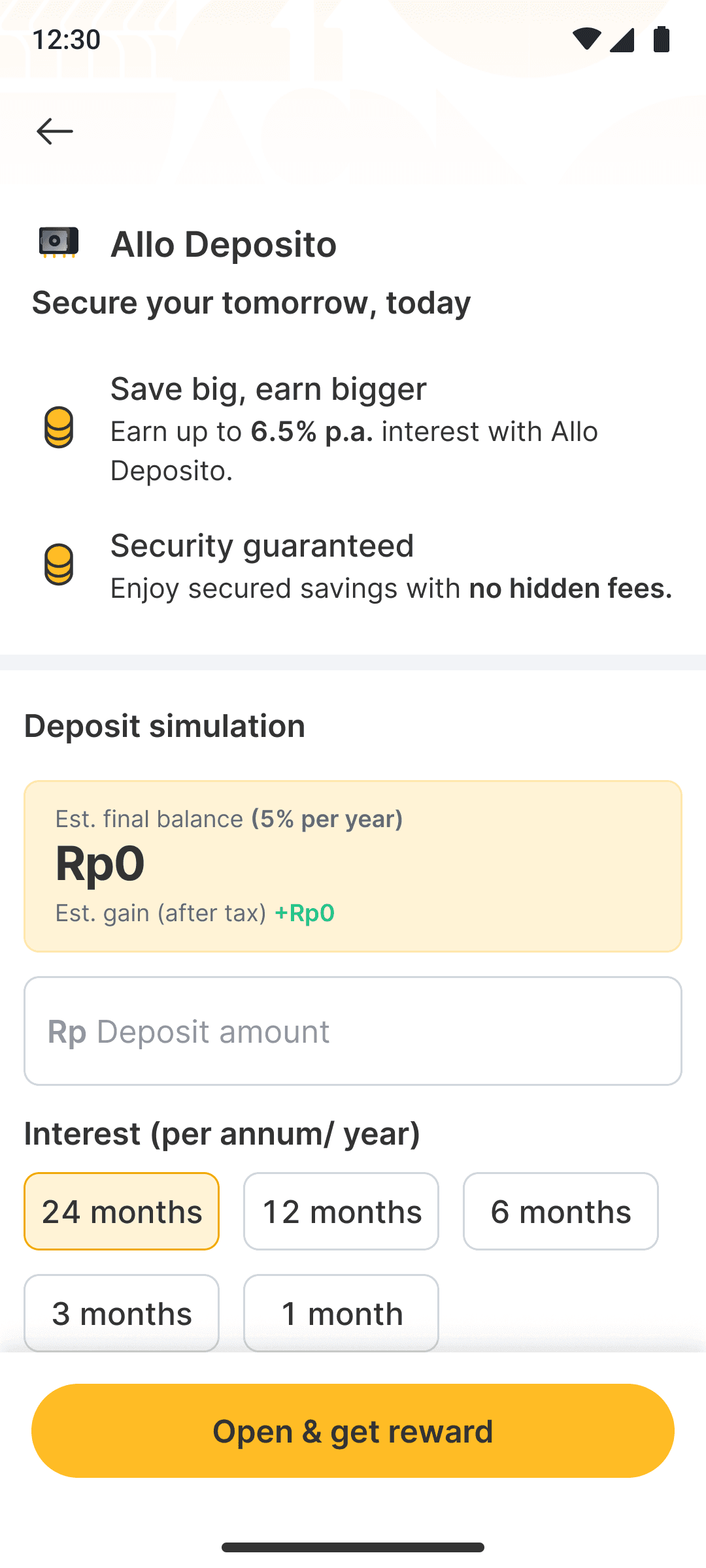

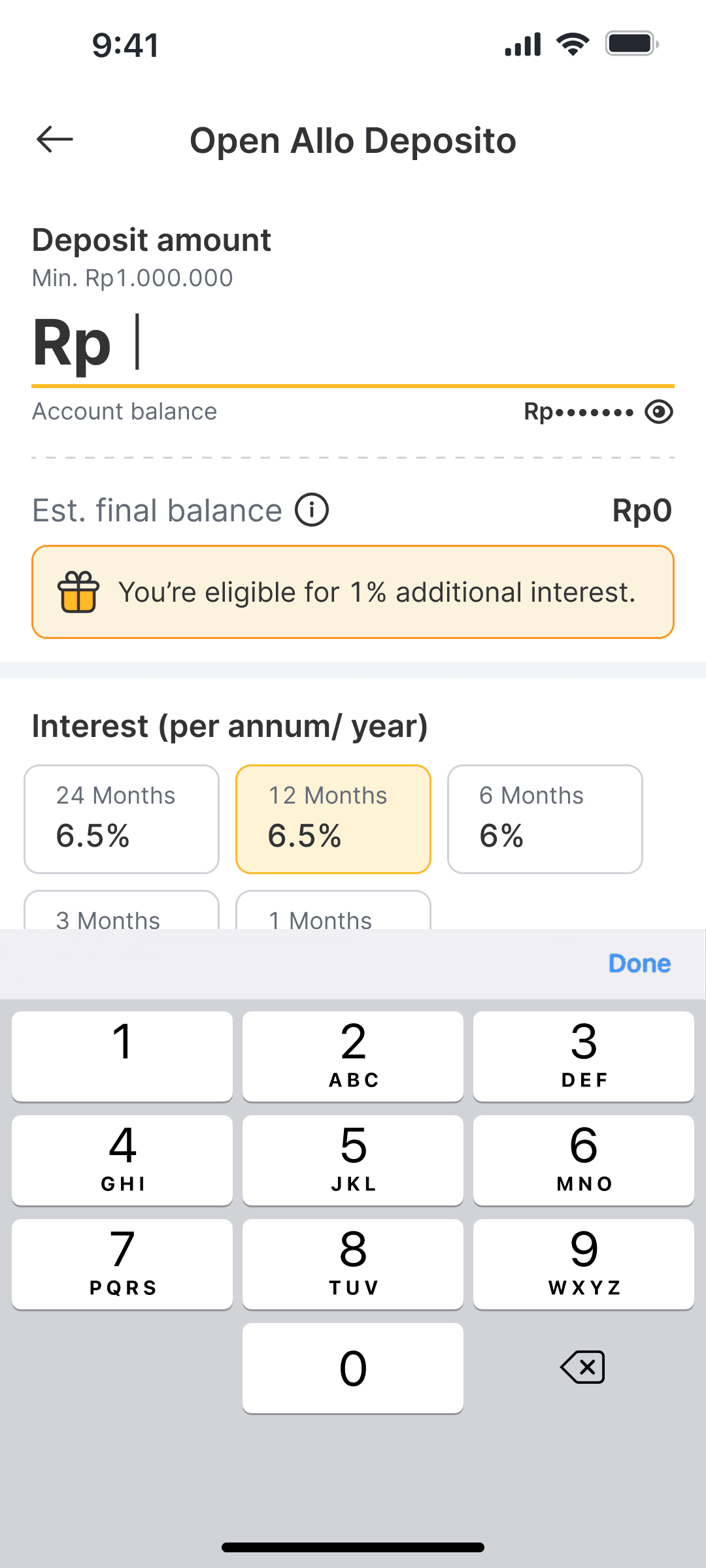

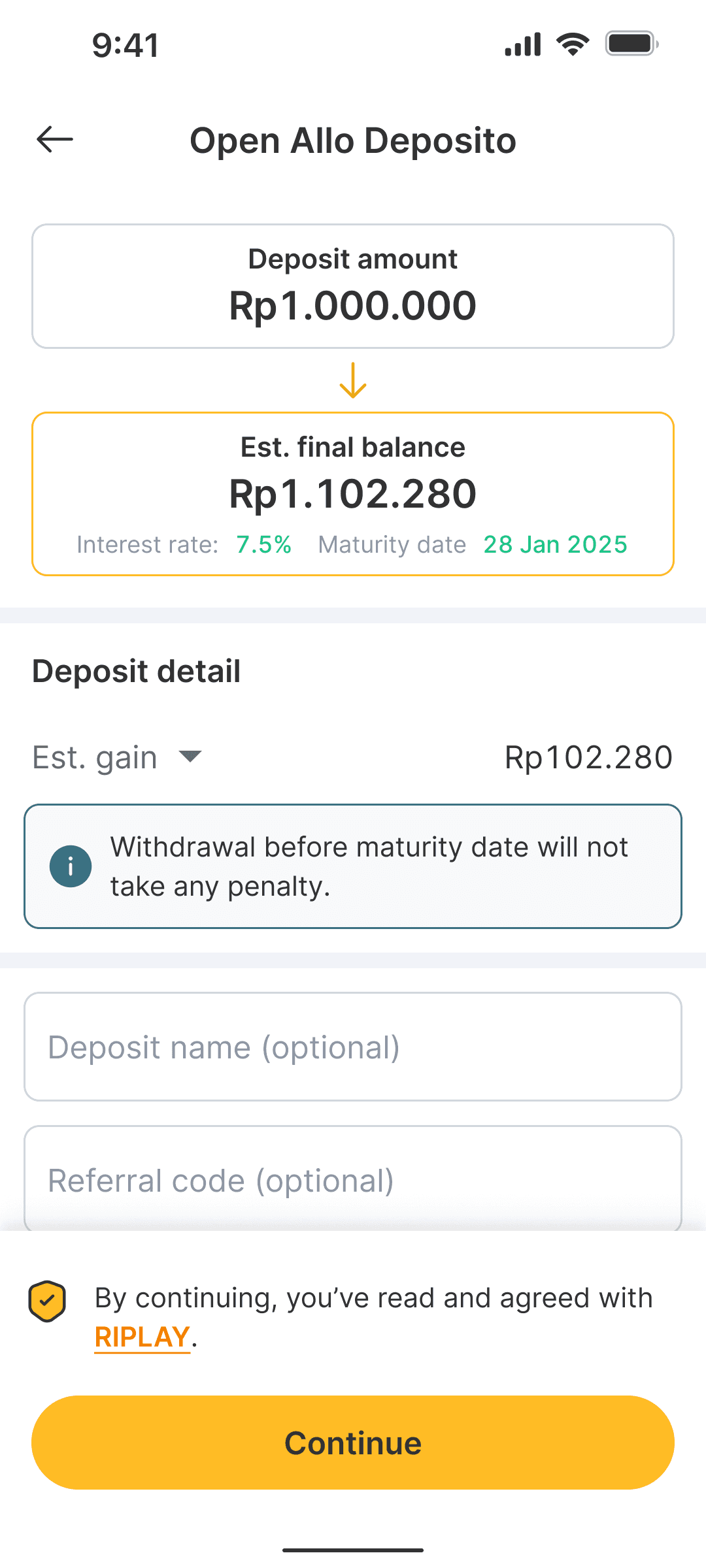

I’ve highlighted the deposit account opening flow, showcasing the revamped design aimed at improving user experience and engagement. Below are the UI screens for the complete flow:

I’ve highlighted the deposit account opening flow, showcasing the revamped design aimed at improving user experience and engagement. Below are the UI screens for the complete flow:

I’ve highlighted the deposit account opening flow, showcasing the revamped design aimed at improving user experience and engagement. Below are the UI screens for the complete flow:

Landing Page.

Input amount.

Amount filled.

Confirmation

Terms and conditions.

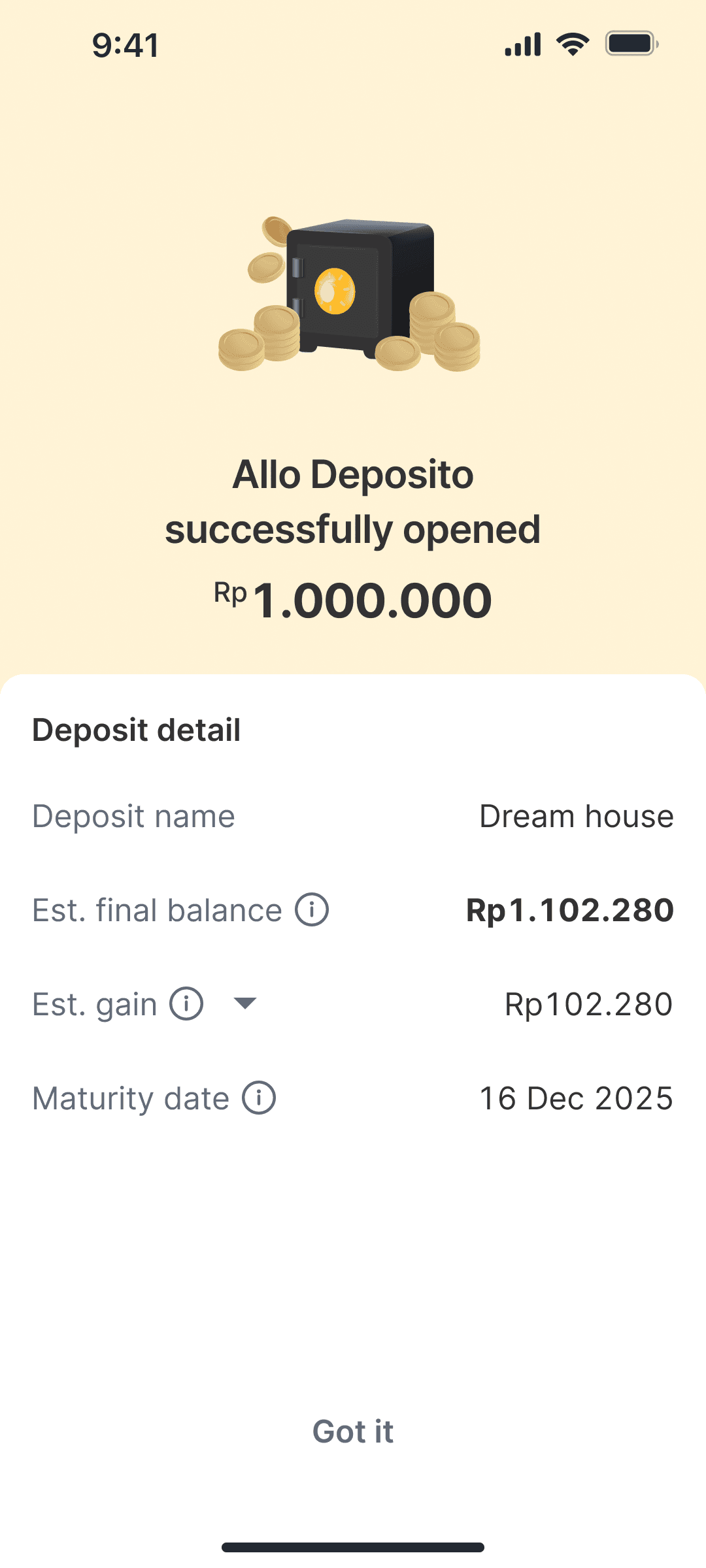

Success.

Opening details.

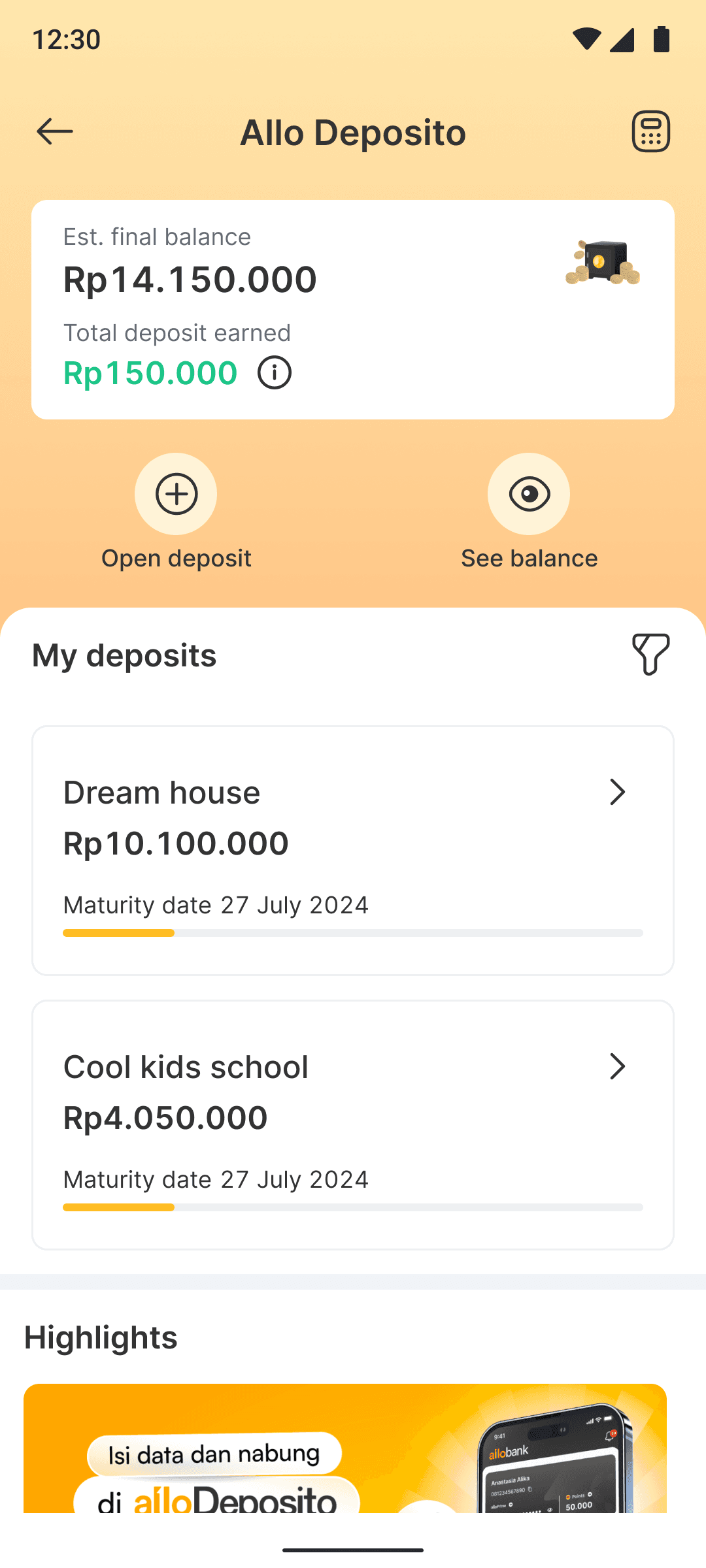

List of deposits.

Landing Page.

Input amount.

Amount filled.

Confirmation

Terms and conditions.

Success.

Opening details.

List of deposits.