For the national UI/UX competition GEMASTIK XII, I co-created Beruang, a personal budget and payment gateway app, with two friends, winning Gold.

For the national UI/UX competition GEMASTIK XII, I co-created Beruang, a personal budget and payment gateway app, with two friends, winning Gold.

For the national UI/UX competition GEMASTIK XII, I co-created Beruang, a personal budget and payment gateway app, with two friends, winning Gold.

Problem statement

Problem statement

Problem statement

In Indonesia, the rise of e-wallets like Go-Pay, OVO, and DANA has made transactions more convenient but also led to impulsive spending and financial instability among users. Many people struggle to manage their finances due to easy access and frequent small purchases. This project addresses these challenges by integrating budgeting tools within e-wallets to promote better financial control.

In Indonesia, the rise of e-wallets like Go-Pay, OVO, and DANA has made transactions more convenient but also led to impulsive spending and financial instability among users. Many people struggle to manage their finances due to easy access and frequent small purchases. This project addresses these challenges by integrating budgeting tools within e-wallets to promote better financial control.

In Indonesia, the rise of e-wallets like Go-Pay, OVO, and DANA has made transactions more convenient but also led to impulsive spending and financial instability among users. Many people struggle to manage their finances due to easy access and frequent small purchases. This project addresses these challenges by integrating budgeting tools within e-wallets to promote better financial control.

E-wallet promotion banner in 2019

E-wallet promotion banner in 2019

E-wallet promotion banner in 2019

Design process

Design process

Design process

To provide the upcoming need, we aim to create a solution that could be predicted and measureable using User-Centered Design method. We also wanted to take minimum risk with short time in the development.

To provide the upcoming need, we aim to create a solution that could be predicted and measureable using User-Centered Design method. We also wanted to take minimum risk with short time in the development.

To provide the upcoming need, we aim to create a solution that could be predicted and measureable using User-Centered Design method. We also wanted to take minimum risk with short time in the development.

Establish requirement

Establish requirement

Establish requirement

Design alternatives

Design alternatives

Design alternatives

Build prototype

Build prototype

Build prototype

Evaluate design

Evaluate design

Evaluate design

Quantitative and qualitative research

Quantitative and qualitative research

Quantitative and qualitative research

We created a survey and gathered 285 respondents to see what they think about mobile payment, the results are:

We created a survey and gathered 285 respondents to see what they think about mobile payment, the results are:

We created a survey and gathered 285 respondents to see what they think about mobile payment, the results are:

70%

70%

70%

said mobile payment

makes purchase decision easier

said mobile payment

makes purchase decision easier

said mobile payment

makes purchase decision easier

81%

81%

81%

said mobile payment is a

helpful payment instrument

said mobile payment is a

helpful payment instrument

said mobile payment is a

helpful payment instrument

83%

83%

83%

said mobile payment

makes buying easier

said mobile payment

makes buying easier

said mobile payment

makes buying easier

But we also discovered some adverse statements related to mobile payment.

But we also discovered some adverse statements related to mobile payment.

But we also discovered some adverse statements related to mobile payment.

I often buy things that are not needed.

I often buy things that are not needed.

It is difficult to maintain budgeting commitments.

It is difficult to maintain budgeting commitments.

I have trouble managing multiple e-wallet accounts.

I have trouble managing multiple e-wallet accounts.

There are difficulties in making the right expenditure plan.

There are difficulties in making the right expenditure plan.

I do not have routine expenditure records.

I do not have routine expenditure records.

I often buy things that are not needed.

There are difficulties in making the right expenditure plan.

It is difficult to maintain budgeting commitments.

I have trouble managing multiple e-wallet accounts.

I do not have routine expenditure records.

Finding themes and How Might We framework

Finding themes and How Might We framework

Finding themes and How Might We framework

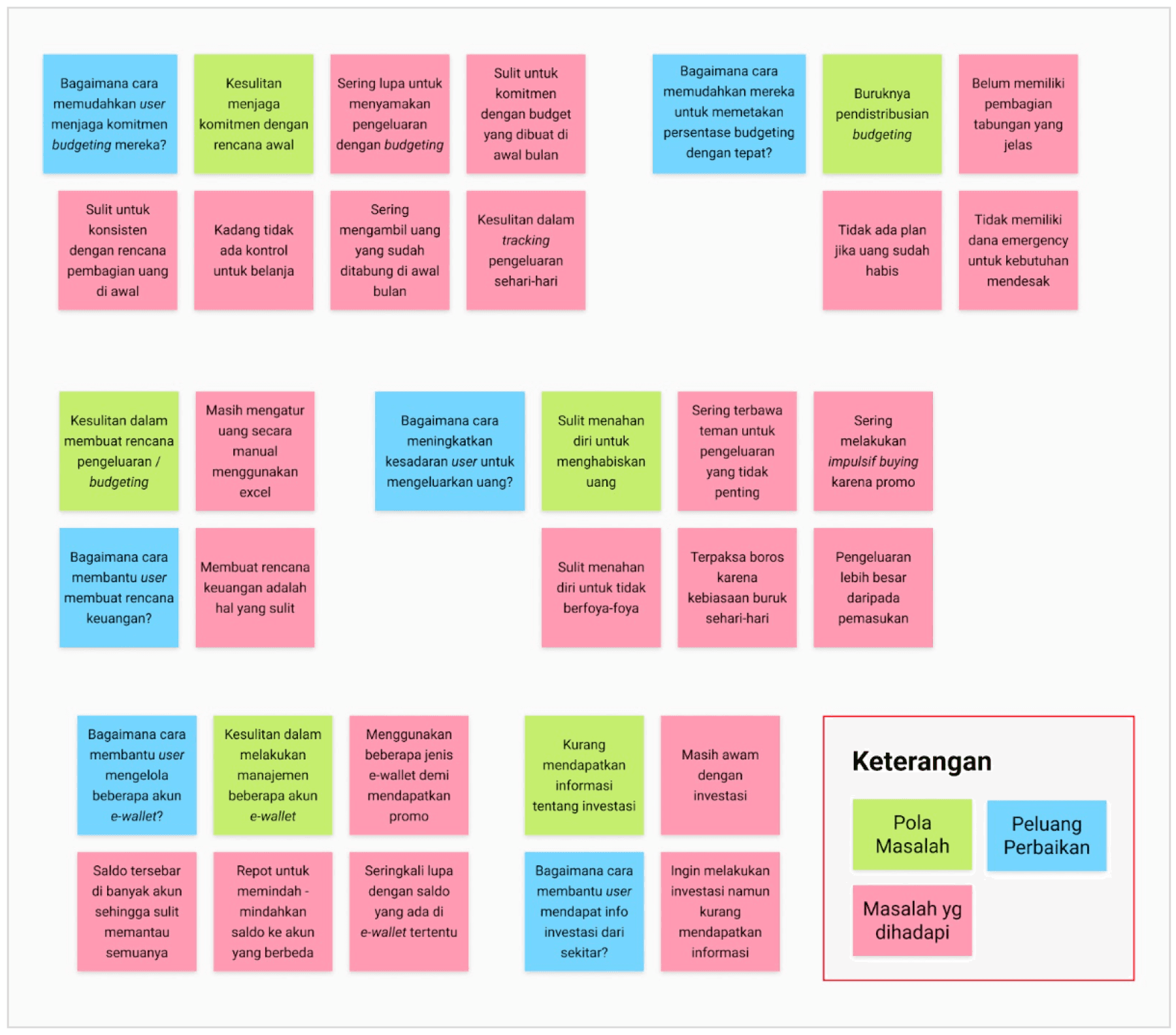

From there, we list problems from interviewees’ statements and insights and group those problem in each theme. After that we create opportunities with How Might We framework.

From there, we list problems from interviewees’ statements and insights and group those problem in each theme. After that we create opportunities with How Might We framework.

From there, we list problems from interviewees’ statements and insights and group those problem in each theme. After that we create opportunities with How Might We framework.

Finding themes

Finding themes

Finding themes

How Might We

How Might We

How Might We

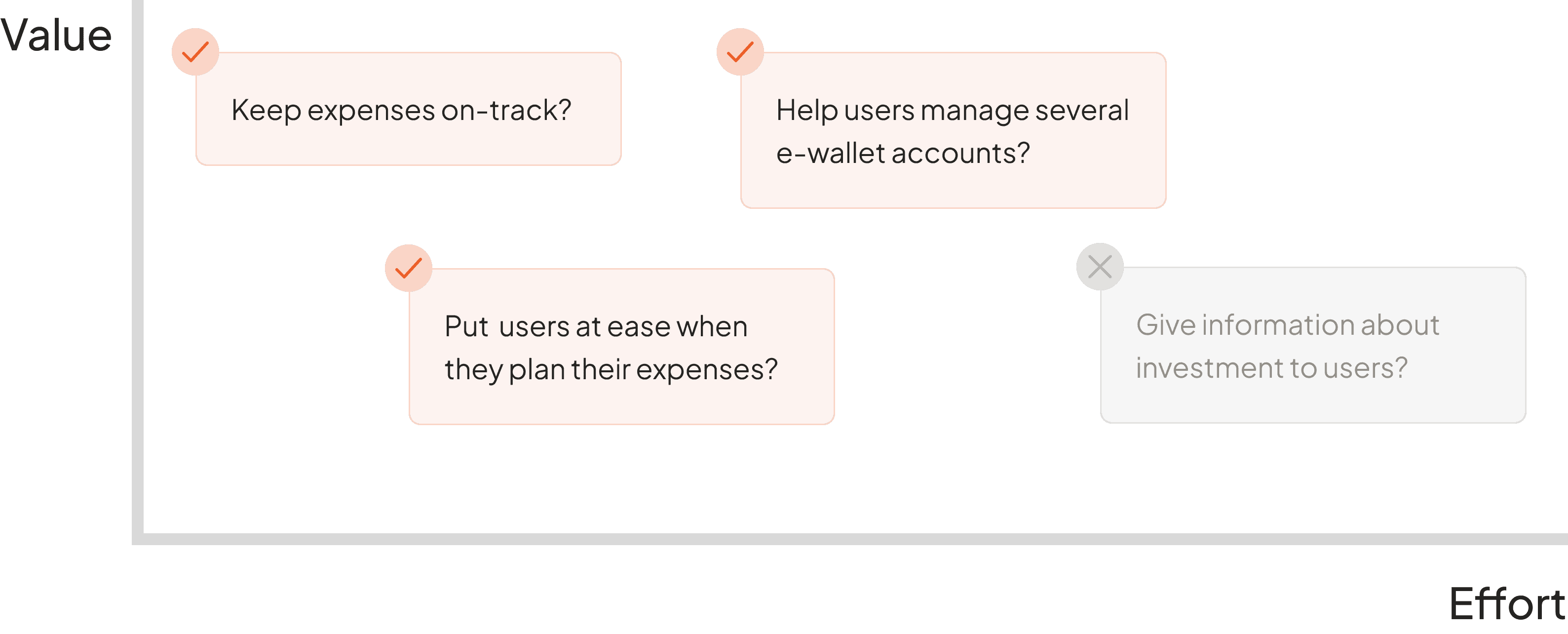

Keep expenses on-track?

Keep expenses on-track?

Give information about investment to users?

Give information about investment to users?

Put users at ease when they plan their expenses?

Put users at ease when they plan their expenses?

Help users manage several e-wallet accounts?

Help users manage several e-wallet accounts?

Put users at ease when they plan their expenses?

Keep expenses on-track?

Give information about investment to users?

Help users manage several e-wallet accounts?

Value-Effort matrix

Value-Effort matrix

Value-Effort matrix

To prioritize on what problem should we answer first, we use Value Effort Matrix. The value defined with how many people felt the problems and how often the problems come. Then, the effort defined with effort to create the solution which in this case, design effort.

To prioritize on what problem should we answer first, we use Value Effort Matrix. The value defined with how many people felt the problems and how often the problems come. Then, the effort defined with effort to create the solution which in this case, design effort.

To prioritize on what problem should we answer first, we use Value Effort Matrix. The value defined with how many people felt the problems and how often the problems come. Then, the effort defined with effort to create the solution which in this case, design effort.

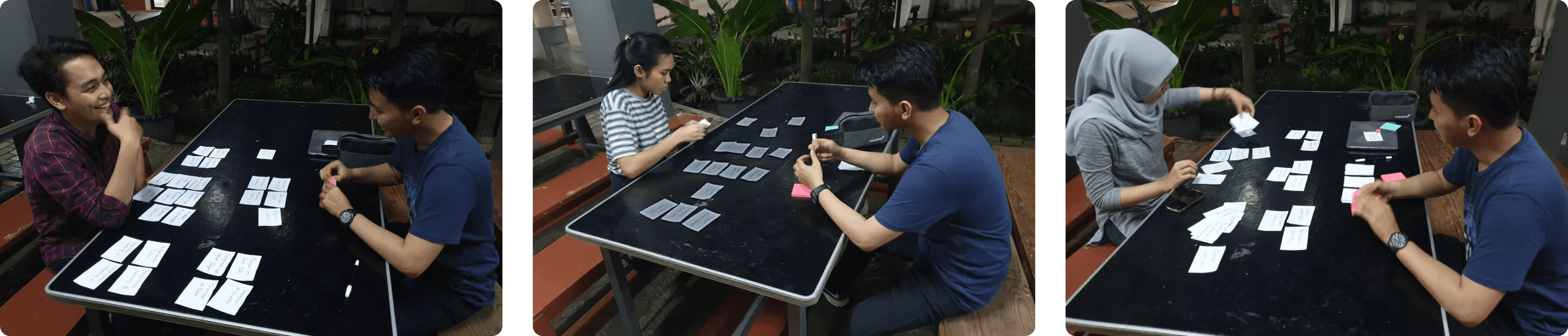

Card Sorting

Card Sorting

Card Sorting

At the beginning of designing alternatives phase, we use card sorting method to understand users mindset when using financial app.

At the beginning of designing alternatives phase, we use card sorting method to understand users mindset when using financial app.

At the beginning of designing alternatives phase, we use card sorting method to understand users mindset when using financial app.

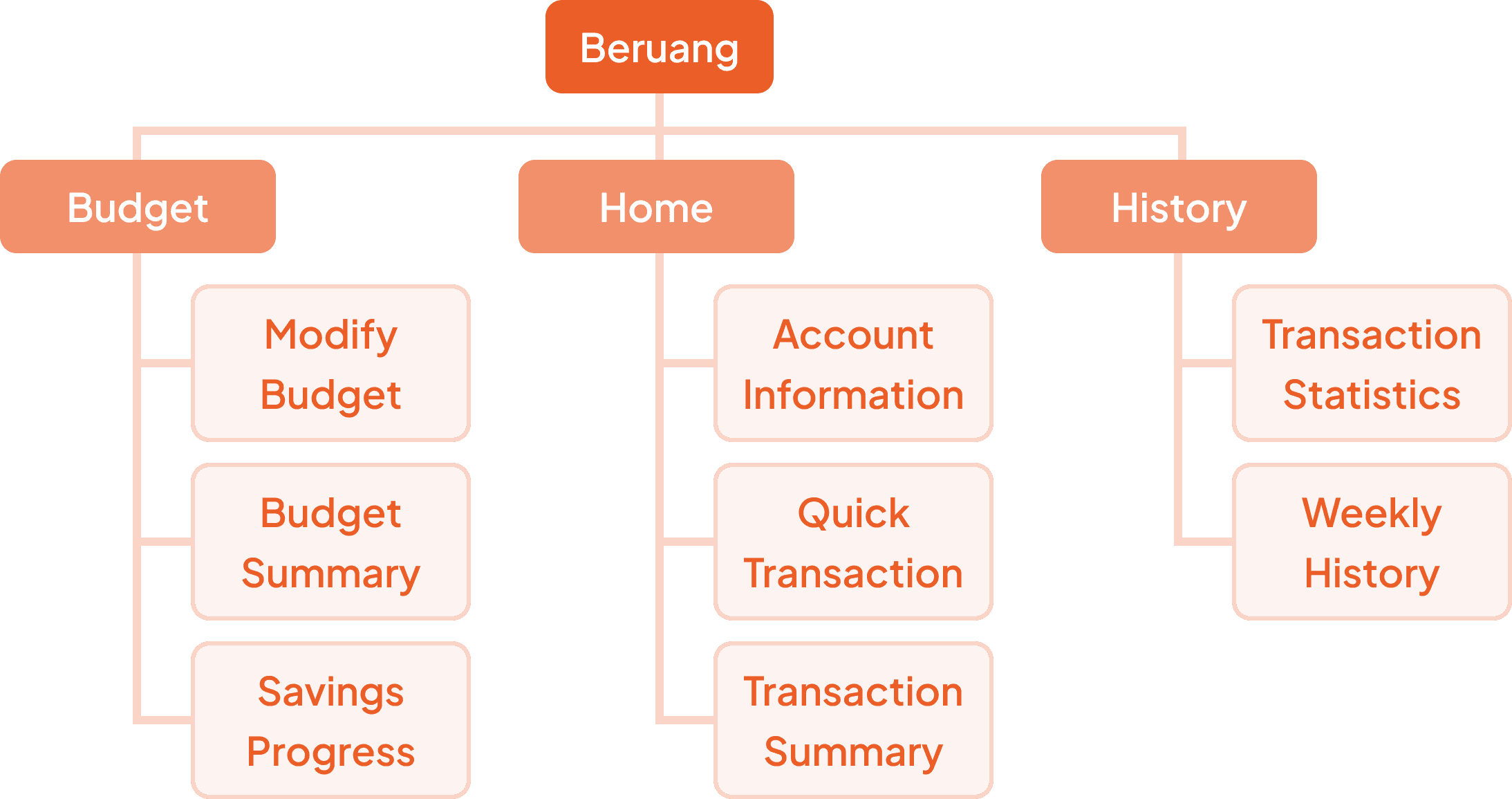

Information Architecture

Information Architecture

Information Architecture

After card sorting, we were provided with adequate information to create Information Architecture.

After card sorting, we were provided with adequate information to create Information Architecture.

After card sorting, we were provided with adequate information to create Information Architecture.

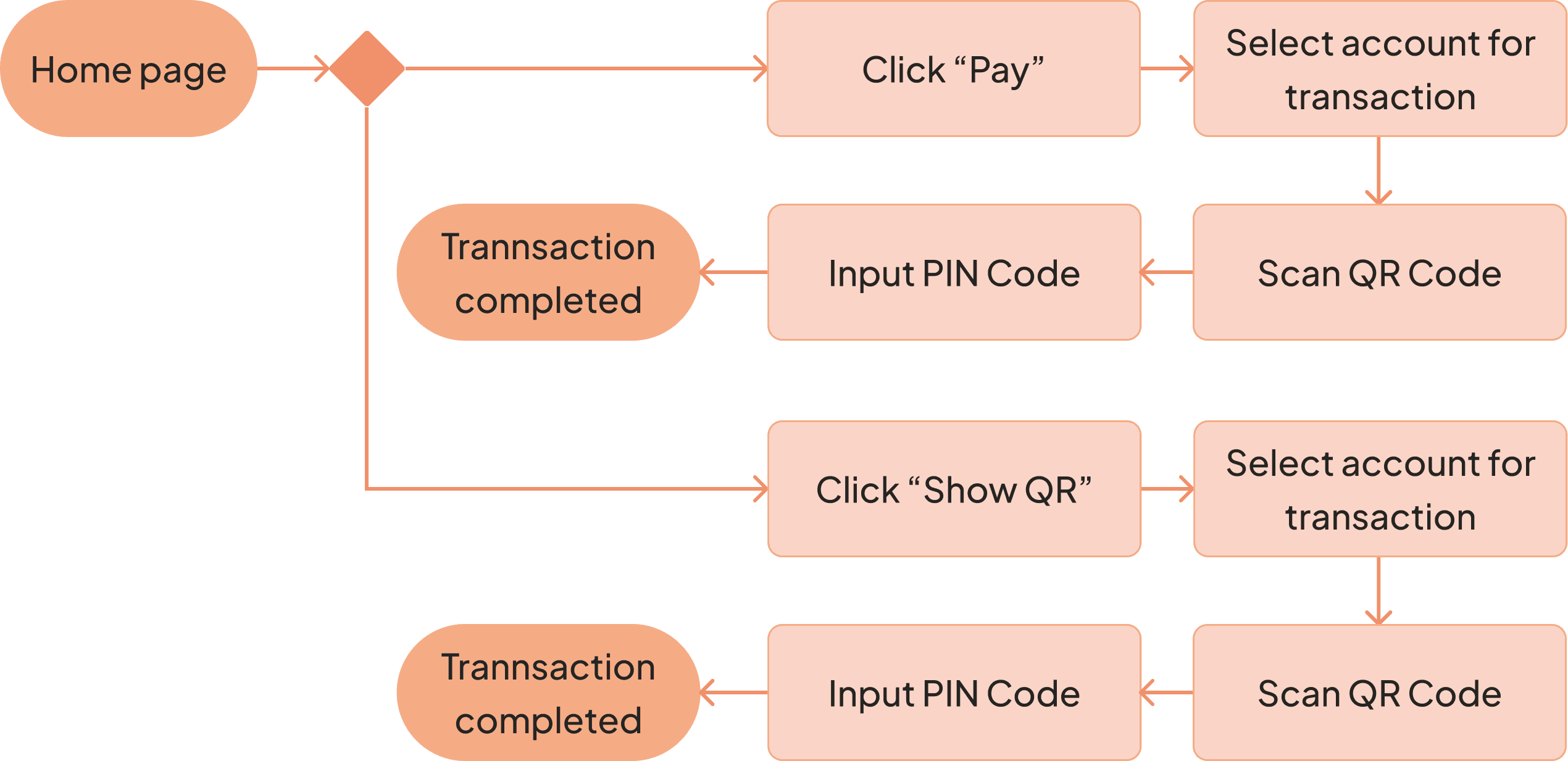

Task Flow

Task Flow

Task Flow

Minimum Viable Product was created with 4 task flow which are:

Minimum Viable Product was created with 4 task flow which are:

Minimum Viable Product was created with 4 task flow which are:

Create monthly budget

Create monthly budget

Create monthly budget

Do daily transcation

Do daily transcation

Do daily transcation

Do transaction above budget

Do transaction above budget

Do transaction above budget

View and share transaction history

View and share transaction history

View and share transaction history

Crazy Eight

Crazy Eight

Crazy Eight

At the prototype phase, we use Crazy Eight method to create fresh ideas on each use case.

At the prototype phase, we use Crazy Eight method to create fresh ideas on each use case.

At the prototype phase, we use Crazy Eight method to create fresh ideas on each use case.

Features

Features

Features

01

01

01

Scan to Pay

Scan to Pay

Scan to Pay

In Scan to Pay, users can view their remaining budget sync with type of expense when conduct a transaction. Scanner also read what type of e-wallet of QR code when it scanned.

In Scan to Pay, users can view their remaining budget sync with type of expense when conduct a transaction. Scanner also read what type of e-wallet of QR code when it scanned.

In Scan to Pay, users can view their remaining budget sync with type of expense when conduct a transaction. Scanner also read what type of e-wallet of QR code when it scanned.

02

02

02

Pay with QR

Pay with QR

Pay with QR

In pay with QR Code, system shows registered user’s e-wallet or mobile banking account. When payment exceeds user’s budget, system automatically suggest to use emergency budget in case user really wanted to make the transaction.

In pay with QR Code, system shows registered user’s e-wallet or mobile banking account. When payment exceeds user’s budget, system automatically suggest to use emergency budget in case user really wanted to make the transaction.

In pay with QR Code, system shows registered user’s e-wallet or mobile banking account. When payment exceeds user’s budget, system automatically suggest to use emergency budget in case user really wanted to make the transaction.

03

03

03

Allocate Budget

Allocate Budget

Allocate Budget

Users can allocate their own budget preferences. Budget also syncronized with user’s periodic balance.

Users can allocate their own budget preferences. Budget also syncronized with user’s periodic balance.

Users can allocate their own budget preferences. Budget also syncronized with user’s periodic balance.

04

04

04

History and Share Receipt

History and Share Receipt

History and Share Receipt

Users can view transaction history on each day and quickly send receipt to friends or family

Users can view transaction history on each day and quickly send receipt to friends or family

Users can view transaction history on each day and quickly send receipt to friends or family

Evaluate design

Evaluate design

Evaluate design

We did Usability Testing and System Usability Scale to evaluate our proposed design. We also asked expert to review our design in business and product aspect.

We did Usability Testing and System Usability Scale to evaluate our proposed design. We also asked expert to review our design in business and product aspect.

We did Usability Testing and System Usability Scale to evaluate our proposed design. We also asked expert to review our design in business and product aspect.

10 Participant, 4 Scenarios

10 Participant, 4 Scenarios

10 Participant, 4 Scenarios

Lesson learned

Lesson learned

Lesson learned

When designed a financial management app, security and user’s trust is a top priority aspect. Users are going to use the app if they feel safe. Users also want the flow to be as easy, simple, and fast as possible so it will not effect their purchase process.

When designed a financial management app, security and user’s trust is a top priority aspect. Users are going to use the app if they feel safe. Users also want the flow to be as easy, simple, and fast as possible so it will not effect their purchase process.

When designed a financial management app, security and user’s trust is a top priority aspect. Users are going to use the app if they feel safe. Users also want the flow to be as easy, simple, and fast as possible so it will not effect their purchase process.